Longevity Risk

With health and well-being at the forefront of everyone’s mind, I believe it is a good time to have a discussion about longevity and the risks it presents to retirees and those close to retirement. This topic has also been discussed in a previous blog about risks retirees face linked HERE.

With medical technology improving at an astounding rate, people who retire at 65 could be looking at 35 years in retirement. With this longer expected lifetime, the question for clients becomes, “Can our money last that long”. This leads to the new idea in the retirement planning world of Longevity Risk Aversion, or the fear someone has about outliving their assets. Rather than using the average life expectancy, which 50% of the population will outlive, we use a life expectancy of 97 of which only about 10% of people will live beyond. Going forward we might have to increase our life expectancy assumptions so that we can make sure our clients will have enough money to last through their retirement given that longevity will increase over time.

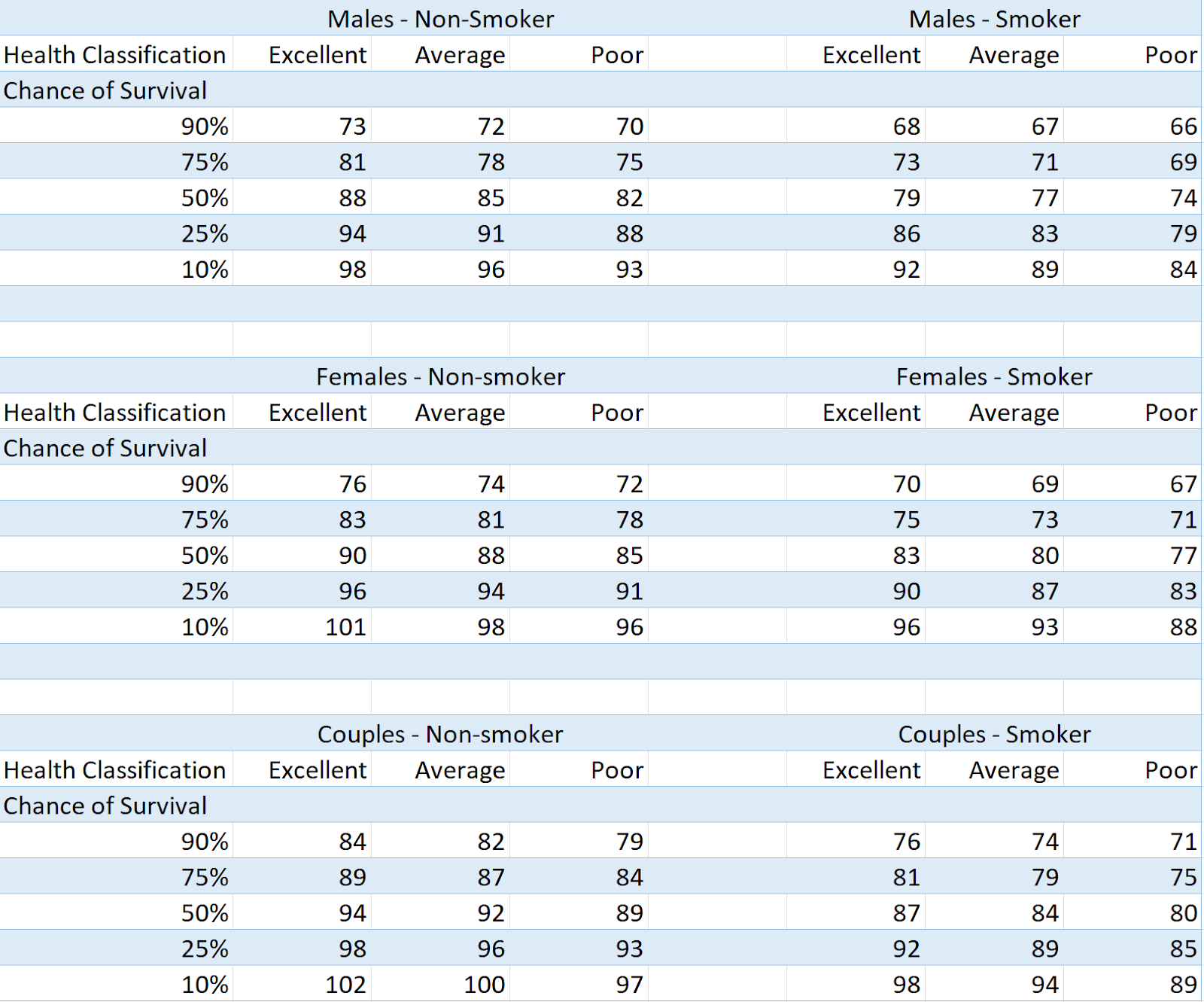

Longevity is dependent on an individuals’ habits, health, family health history, and other socioeconomic characteristics that correlate with mortality – it is up to each person, in consultation with their financial professional, to include these assumptions in their retirement plan. For example, if a client has poor health and has family health issues, they might want to front load their distributions to enjoy the rewards of their years of work while they can. While someone who is healthy and had parents who lived well past the averages might want to back load distributions to make sure they do not run out of money while still alive. Below are example charts of life expectancy. If you would like to see your personal longevity illustration, please visit LongevityIllustrator.org.

American Academy of Actuaries and Society of Actuaries, Actuaries Longevity Illustrator, http://www.longevityillustrator.org/, (accessed Dec., 4, 2021).